Introducing gogocoin — A Self-Hosted Crypto Trading Bot

Why I Built It

Open-source crypto bots and automated trading services are everywhere. I built gogocoin anyway because I wanted the hands-on experience of implementing something that works exactly as I intend and actually earning returns with my own money. I had built a similar bot once before; this time I rebuilt it from scratch with the help of AI. Running it in production has been a continuous source of learning — it has become a hobby as much as a software project.

Getting Started

gogocoin is bitFlyer-only. All exchange communication goes through the author's own go-bitflyer-api-client library; no other exchange works. The bot places orders via bitFlyer's spot-only endpoint (/v1/me/sendchildorder), so margin / futures trading (e.g. FX_BTC_JPY) does not work.

There are two ways to use gogocoin.

A. Use as a library (recommended)

example/ is a fully working sample and a starting point for your own repo.

git clone https://github.com/bmf-san/gogocoin.git && cd gogocoin/example

# Create config and set API credentials via environment variables

cp configs/config.example.yaml configs/config.yaml

export BITFLYER_API_KEY=your_key

export BITFLYER_API_SECRET=your_secret

make run

# or: go run ./cmd/

# → Dashboard at http://localhost:8080

Using example/configs/config.example.yaml as-is, the bot runs an XRP/JPY scalping strategy with a 1000 JPY order size. Adjust trading.symbols and strategy_params.scalping.order_notional to trade different pairs or sizes. The bot stores trade data in SQLite (no external database needed).

You can also integrate gogocoin into your own module via go get github.com/bmf-san/gogocoin@latest.

B. Docker for quick testing

example/ includes a Dockerfile and docker-compose.yml that build a fully working binary with the same EMA+RSI scalping strategy registered.

git clone https://github.com/bmf-san/gogocoin.git && cd gogocoin/example

cp configs/config.example.yaml configs/config.yaml

# Edit configs/config.yaml and set your API credentials

make up

# → Dashboard at http://localhost:8080

The Dockerfile build context is the repo root, so run make up from the example/ directory.

Architecture

The codebase follows a four-layer architecture. internal/ houses domain logic, use cases, and external adapters (bitFlyer client, SQLite repository, HTTP handlers, etc.); pkg/strategy is a public package providing the Strategy interface definition and a scalping reference implementation. The Composition Root (wiring all services together) lives in the caller's repository — example/cmd/main.go is a working sample.

C4 Context — System Overview

C4 Container — Main Containers

C4 Component — usecase/trading

Dependency Graph

Dependency rules are enforced in CI:

| Rule | Detail |

|---|---|

domain/ has zero internal imports |

stdlib only; knows nothing of infra or usecase |

usecase/ does not import infra/ |

depends only on domain/ interfaces |

adapter/ holds no concrete infra types |

uses domain/ interfaces only |

infra/ implements domain/ |

knows nothing of usecase/ or adapter/ |

| Composition Root lives in the caller's repository | internal/ needs no wiring |

The public API (subject to semantic versioning) lives under pkg/. pkg/engine is the engine entry point; pkg/strategy provides the Strategy interface and registry.

Use Cases

The operator controls and monitors the bot via the HTTP API (including the web dashboard). Signal generation, order placement, P&L calculation, and data cleanup run autonomously.

Trading Flow

The following shows the main path from receiving a WebSocket tick to filling an order and recording P&L.

6.1 Scalping Trading Flow

StrategyWorker and SignalWorker are connected asynchronously via a Go channel. PlaceOrder() returns immediately after placing the order; OrderMonitor handles fill monitoring in a goroutine. PnLCalculator saves position and trade records within the same transaction; OrderMonitor appends the balance snapshot separately after that completes.

6.2 REST API Trading Control Flow

6.3 Market Data Collection Flow

6.4 Order Timeout / CANCELED•EXPIRED Flow

6.5 Rate Limit Retry Flow

6.6 MaintenanceWorker Flow

Strategy Interface

Every trading strategy follows the Strategy interface defined in pkg/strategy/strategy.go. This keeps the engine decoupled from any specific algorithm:

// AutoScaleConfig holds the order-size auto-scaling parameters returned by

// Strategy.GetAutoScaleConfig. The engine uses this to compute buy notional

// without reading strategy-specific config keys directly.

type AutoScaleConfig struct {

Enabled bool

BalancePct float64 // % of available JPY balance to use (0-100)

MaxNotional float64 // hard cap in JPY; 0 = unlimited

FeeRate float64

}

type Strategy interface {

// GenerateSignal generates a signal from the latest market data point and

// the historical series for the same symbol.

GenerateSignal(ctx context.Context, data *MarketData, history []MarketData) (*Signal, error)

// Analyze generates a signal from a batch of historical data.

Analyze(data []MarketData) (*Signal, error)

// Lifecycle

Start(ctx context.Context) error

Stop(ctx context.Context) error

IsRunning() bool

GetStatus() StrategyStatus

Reset() error

// Metrics & trade accounting

GetMetrics() StrategyMetrics

RecordTrade()

InitializeDailyTradeCount(count int)

// Configuration

Name() string

Description() string

Version() string

Initialize(config map[string]interface{}) error

UpdateConfig(config map[string]interface{}) error

GetConfig() map[string]interface{}

// Order sizing — each strategy owns this logic so the engine never reads

// strategy-specific config keys directly.

GetStopLossPrice(entry float64) float64 // 0 = no stop-loss

GetTakeProfitPrice(entry float64) float64 // 0 = no take-profit

GetBaseNotional(symbol string) float64

GetAutoScaleConfig() AutoScaleConfig

}

Initialize() receives the strategy_params.<name> block from config.yaml as a map[string]interface{}. UpdateConfig() allows live parameter updates via the HTTP API without restarting the bot.

Strategies self-register via the global registry using the same mechanism as database/sql driver registration. A register.go file in each strategy package calls strategy.Register("name", constructor) inside init(), and main.go pulls the strategy in with a blank import (_ "github.com/bmf-san/gogocoin/pkg/strategy/scalping"). Adding a new strategy is an import change in main.go — no engine code needs to change.

Engine Risk Management

The engine (StrategyWorker) enforces stop-loss and take-profit on every market tick, independently of any signal. It calls GetStopLossPrice / GetTakeProfitPrice on each tick and closes the position immediately when the price crosses the threshold — no signal required.

A max_open_positions_per_symbol: 1 guard in config.yaml prevents position stacking. Without it, consecutive BUY signals during a downtrend accumulate multiple open positions on the same symbol, and when stop-loss fires all of them close simultaneously, multiplying the loss. With the guard set to 1, any BUY is rejected if the symbol already has an open position.

The engine also supports balance-proportional order sizing as a framework feature via GetAutoScaleConfig(). To enable it, override GetAutoScaleConfig() in your own strategy to return Enabled: true with a BalancePct and optional MaxNotional.

Balance Cache — Double-Checked Locking

The trading loop polls account balance frequently. Calling the bitFlyer REST API on every tick would quickly exhaust the rate limit of 50 requests per minute. BalanceService caches the result with a 60-second TTL and uses a double-checked locking pattern to prevent thundering-herd API calls when the cache expires:

func (s *BalanceService) GetBalance(ctx context.Context) ([]domain.Balance, error) {

// First check: read without write lock

s.cache.mu.RLock()

cacheTimestamp := s.cache.timestamp

cacheData := s.cache.data

s.cache.mu.RUnlock()

if time.Since(cacheTimestamp) < CacheDuration && len(cacheData) > 0 {

result := make([]domain.Balance, len(cacheData))

copy(result, cacheData)

return result, nil

}

// Serialize fetches: only one goroutine calls the API at a time

s.fetchMu.Lock()

defer s.fetchMu.Unlock()

// Second check: re-verify after acquiring the lock

s.cache.mu.RLock()

cacheTimestamp = s.cache.timestamp

cacheData = s.cache.data

s.cache.mu.RUnlock()

if time.Since(cacheTimestamp) < CacheDuration && len(cacheData) > 0 {

result := make([]domain.Balance, len(cacheData))

copy(result, cacheData)

return result, nil

}

// ... call API and update cache

}

The outer cache.mu (a sync.RWMutex) allows concurrent reads of fresh cache data. The inner fetchMu (a sync.Mutex) serialises API calls so that exactly one goroutine fetches when the cache is stale.

Data Model

Trade data is persisted in SQLite. The table-to-domain-model mapping:

| Table | Content | Notes |

|---|---|---|

trades |

Filled order records | order_id UNIQUE for idempotency. Immutable (no UPDATE) |

positions |

FIFO positions | 3 states: OPEN / PARTIAL / CLOSED. Created on BUY, updated on SELL |

balances |

Balance snapshots | Append-only (no overwrites). Latest row per currency |

market_data |

WebSocket tick data | UNIQUE(symbol, timestamp) |

performance_metrics |

Daily performance metrics | Snapshot appended after each fill |

logs |

Structured log entries | fields column is JSON |

app_state |

Runtime flag KV store | e.g. trading_enabled |

No foreign key constraints are defined. The only cross-table logical reference is between positions and trades, but PnLCalculator writes both within the same transaction (BeginTx → SavePosition/UpdatePosition → SaveTrade → Commit). Transaction atomicity guarantees consistency, making DB-level FK constraints unnecessary.

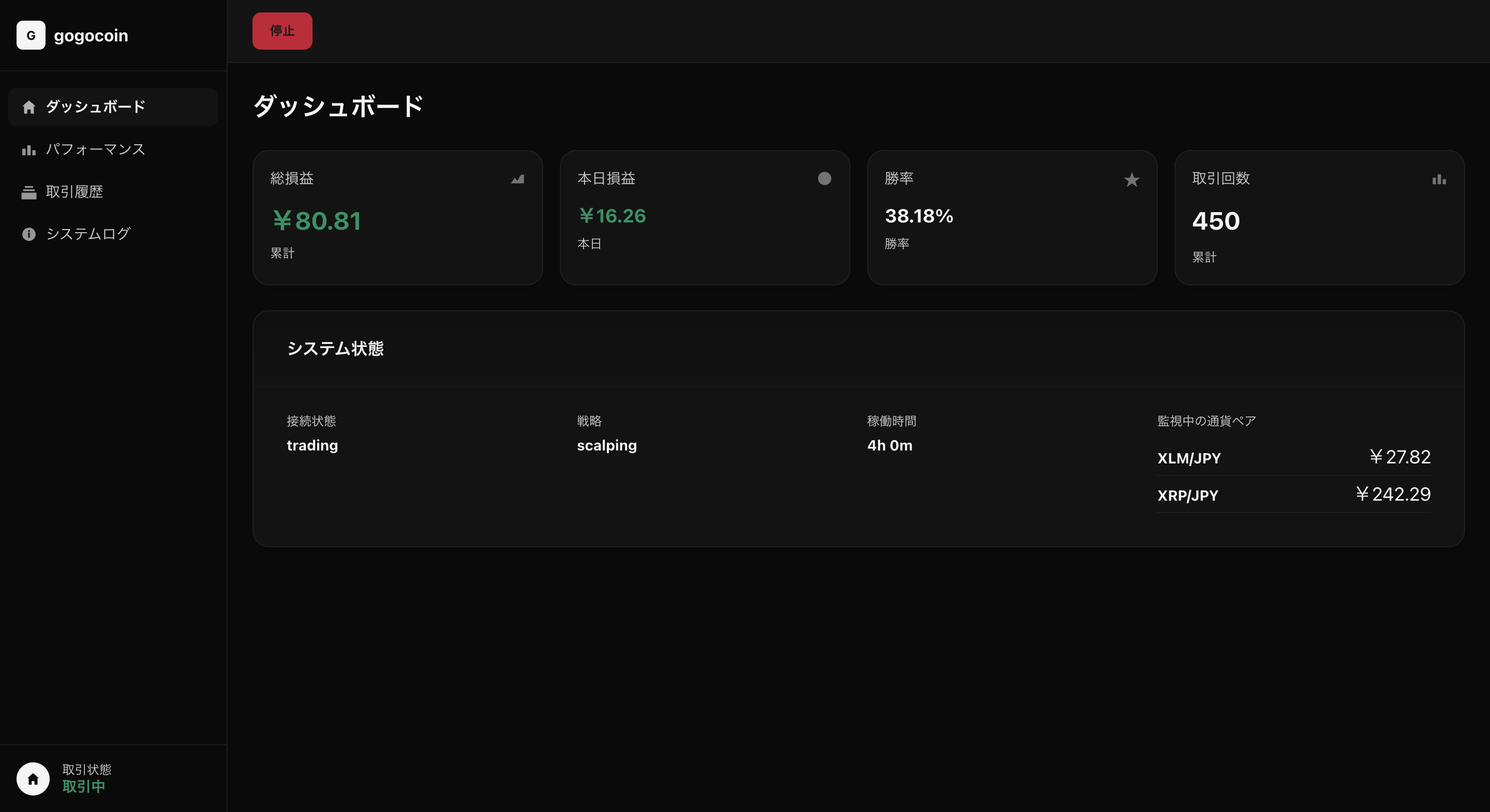

Web Dashboard

The embedded web UI at http://localhost:8080 has four pages, navigable via the sidebar.

- Dashboard — Four summary cards (total P&L, today's P&L, win rate, daily trade count) plus a system status panel showing connection state, active strategy, uptime, and live prices for monitored currency pairs.

- Performance — Per-currency balance table (total / available), three risk metrics (Sharpe ratio, profit factor, max drawdown), and a daily P&L history table.

- Trade History — Full trade log with timestamp, currency pair, side, price, size, fee, and P&L columns.

- System Logs — Log viewer filterable by level (DEBUG / INFO / WARN / ERROR) and category (system / trading / API / strategy / UI / data).

Start and stop buttons in the top bar control the bot in real time. Configuration (API credentials, trading parameters) lives in config.yaml. The bot writes data to SQLite — no external database required.

Running in Production

gogocoin ships as a single statically-linked binary. gogocoin-vps-template is a sample reference for running it on ConoHa VPS, covering systemd configuration and deployment steps.

Initial VPS setup (systemd service installation, etc.) uses make setup. Ongoing deployment is automated via the included GitHub Actions workflow (workflow_dispatch), which builds for linux/amd64 and transfers the binary to the VPS with rsync.

Summary

gogocoin is a minimal self-hosted trading bot that lets you freely implement your own trading strategy and run it with real money. Having your own code directly tied to real P&L is genuinely exciting — and there is no end to how deep you can go tuning strategies and building new features. If any of this sounds interesting, feel free to give it a try.

- GitHub: bmf-san/gogocoin

- VPS Template: bmf-san/gogocoin-vps-template